Credit Strong Review [2025]

By Maddy Scheckel

By Maddy Scheckel It’s that time of the year again.

You spent the last few months finding the perfect gifts for your loved ones.

Like many Americans, who account for over $1 trillion of credit card debt, you overspent (again). This likely means your credit score is going to take a hit (again).

You wanted to start this year off in better financial shape, but you’re not sure where to start.

One option is to use Credit Strong. It’s an online service that offers credit builder loans to boost credit scores.

Before signing up for Credit Strong, you need to know how it works and if it’s legit. This Credit Strong review will explain all of that – and more!

What is Credit Strong?

Credit Strong is a financial technology business that uses credit builder loans to help people build credit. It’s a division of Austin Capital Bank, which is a member of the FDIC (Federal Deposit Insurance Corporation), and it has over 1 million clients.

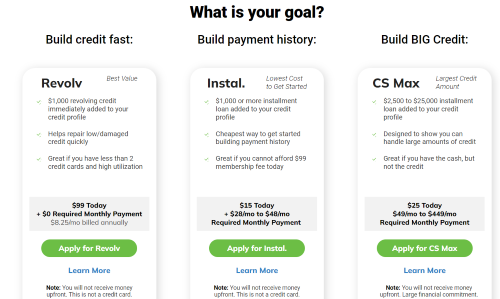

Credit Strong offers three different credit-building products:

- Revolv – This is a $1,000 line of credit that lowers your “credit utilization” to lift your credit score. It costs $99 per year.

- Instal – This is a classic credit-builder loan. You’ll make monthly payments and then receive the loan amount at the end. Plans range from $28 – $48 per month, and you’ll also pay interest and a one-time fee of $15.

- CS Max – This is for plus-size credit builder loans that can last up to 60 months. The monthly payments range from $49 – $449, depending on the size of the loan, and the maximum loan amount is $25,000.

You can use just one of these products – or combine Revolv with one of the other two Credit Strong plans (Instal or CS Max).

Source: Credit Strong

How Does Credit Strong Work?

It’s time for this Credit Strong review to break down each of the available plans.

Let’s start with Revolv, Credit Strong’s revolving credit product.

Here’s how Revolv works:

- You get a $1,000 revolving line of credit. It’s basically like a credit card, except in this case, you won’t use the credit to make purchases. The idea here is to build credit, not borrow funds. Credit Strong will then report this line of credit to the three major credit bureaus. The extra available credit means your “credit utilization” will go down – which should bring your credit score up.

- You make optional additional payments to further build credit. These payments can be $20 – $90 per month (or between 2% and 9% of your Revolv credit limit). They’ll contribute to your savings while also adding payment history to your credit report, which should lift your credit score.

- Increase your credit limit to $3,000. While the initial line of credit is only $1,000, it can rise to $3,000 if you consistently make savings payments on time. The increased limit should help your credit score go even higher.

All of this costs just $99 per year, with no additional fees or interest charges to worry about. There’s also no hard credit check, making it quick and easy to sign up. You can cancel Revolv at any time.

Credit Strong’s other two products, Instal and CS Max, are both credit builder loans. What distinguishes them is their size. Instal is a low-cost credit-building option, while CS Max is for people willing to throw some serious money into the credit-building process.

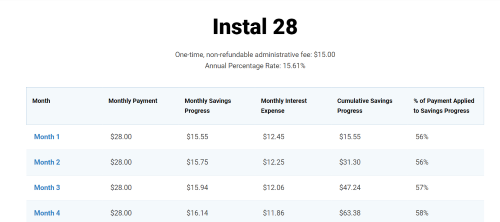

So let me break down Instal for you. It’s a standard credit builder loan, and here’s how it works:

- You open your account. This shouldn’t take long since there’s no credit check required.

- You pick your plan. There are three plans available, costing $28 per month, $38 per month, or $48 per month, respectively. The more you pay, the faster you’ll set money aside and the sooner you’ll get the money back.

- Make monthly payments to pay off the loan. And no – this isn’t a loan where you’ll actually get the money. But that’s the idea! Credit Strong will report your on-time payments, which should improve your credit score.

- Collect your savings. Once you’ve paid off the entire amount of the loan, you’ll get most of the money back. You can also cancel at any time to get your money sooner. The only cost will be the interest paid on the loan and a one-time $15 fee.

Instal is basically a loan in reverse. Instead of getting money and then paying it back, you pay money and then receive most of it again later. But the upshot is that your credit score should improve in the process!

Then there’s CS Max, which is like Instal on steroids. I won’t lay out the step-by-step process since it’s almost the same as with Instal. What matters here are the costs – and they’re pretty hefty.

CS Max offers four different plans:

- $49 per month (for a $2,500 loan)

- $99 per month (for a $5,000 loan)

- $199 per month (for a $10,000 loan)

- $448 per month (for a $25,000 loan)

You’ll also have to pay interest and a $25 one-time fee. And with such high loan amounts, the interest will add up quickly. That means CS Max is not a low-cost way to build credit.

CS Max is designed for unique circumstances, like an entrepreneur who wants to build personal credit for their business or a consumer who desperately needs credit cards with higher credit limits. Even then, you need to have the cash on hand to make the large monthly payments.

Source: Credit Strong

Is Credit Strong Legit?

Credit Strong is a totally legitimate enterprise. It’s part of Austin Capital Bank, which is a reputable savings bank based in Texas.

Unfortunately, not all customers are satisfied with Credit Strong. It only gets an average of 2.6 stars from users on Trustpilot.

But here’s the good news: That average comes from a sample size of just 36 Trustpilot reviews. Considering the legitimacy of Credit Strong’s parent institution, I think it’s safe to call it trustworthy.

![]() Don’t Miss This:

Don’t Miss This:

Is Credit Strong Safe?

Credit Strong is totally safe to use because the first $250,000 in all of its accounts is protected by the government.

Remember, Credit Strong is a division of Austin Capital Bank, which is a member of the FDIC. So, even if the bank were to fail and your money disappeared, the federal government would pay you back. How’s that for reassurance?

Now, if you’re looking for other safe ways to improve your credit, check out this list of the best credit repair companies.

Pros and Cons of Credit Strong

Credit Strong is a reputable service with a lot to like – but it comes with costs and limitations, too. It’s time for this Credit Strong review to break down the pros and cons.

Pros

- Credit Strong reports to all three credit bureaus. That makes it more likely that your credit score will rise.

- There’s no credit check when signing up. And since your credit score is probably a little iffy (or you wouldn’t be considering these products!), this is seriously great news.

- There are lots of credit-building options. Credit Strong offers three different products, and you’ll have flexibility in how much you pay.

Cons

- There’s no Credit Strong mobile app. Some other credit builders offer an app-based model.

- The products can be expensive. The revolving line of credit costs $99 a year, while the credit-builder loans come with interest charges and fees.

- Your credit score could take a momentary hit. When credit bureaus see you’ve opened a new credit account, they might ding your credit score. But your credit score should go back up as you make your Credit Strong payments.

Credit Strong Reviews

I found a lot of fascinating Credit Strong reviews on Trustpilot, where real customers share their experiences.

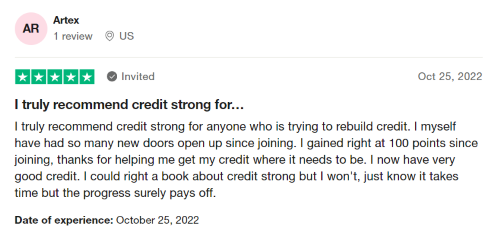

In a 5-star Credit Strong review, someone said their credit score had increased by 100 points.

Source: Trustpilot

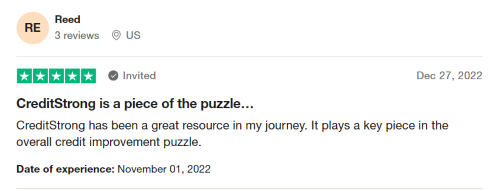

Another customer called Credit Strong “a key piece in the overall credit improvement puzzle.” I really like that wording. It reflects how no one product can single-handedly fix your credit, but a service like Credit Strong can help.

Source: Trustpilot

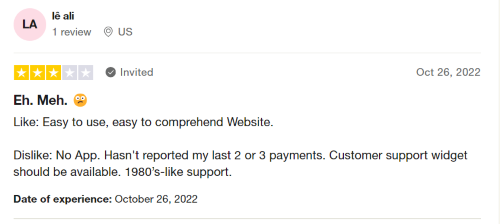

In a 3-star Credit Strong review, someone said they liked the website but disliked the fact that there isn’t a mobile app.

Source: Trustpilot

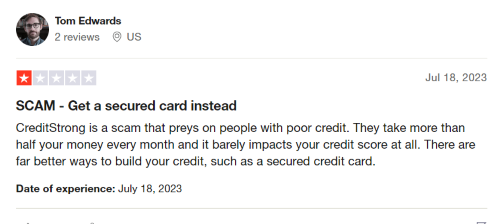

And in a scathing 1-star Credit Strong review, a user claimed the service takes “more than half your money every month.” I’m not sure their math quite checks out, but it’s true that Credit Strong costs more than some competitors.

Source: Trustpilot

Credit Strong Reviews Reddit

Let’s take a look at a Reddit thread where someone asked about Credit Strong. It’s a few years old, but it’s the most detailed Credit Strong conversation I could find on Reddit.

The thread started with someone asking a very simple question: Is Credit Strong good or bad?

Source: Reddit

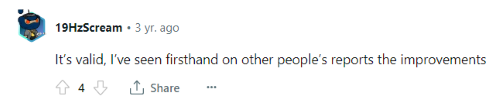

Most people responded positively. One person left a Credit Strong review describing how they’ve seen other people’s credit scores improve.

Source: Reddit

Another person said they were a credit attorney whose clients had succeeded with the service. Now that’s a Credit Strong review you can trust!

Source: Reddit

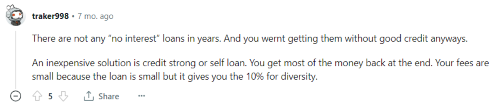

I also found a more recent post (in a different thread) where a Redditor suggested using Credit Strong. They described it as an inexpensive way to build credit.

Source: Reddit

Credit Strong Reviews BBB

The Better Business Bureau (BBB) gives Credit Strong a B grade. This rating is based on the 95 complaints that the BBB has received about the service in the last three years.

Credit Strong’s parent institution, Austin Capital Bank, gets an A+ grade from the BBB. So when you use Credit Strong, you’re working with people you can trust.

Is Credit Strong Worth It?

The verdict of this Credit Strong review is that the service is generally worth it. That said, it’s worth distinguishing between Credit Strong’s “standard” products and their more specialized “CS Max” plans.

The two standard products, Revolv and Instal, are great options for anyone who desperately wants their credit score to improve and has some money to put towards the project.

They’re not free – in fact, they’re not necessarily cheap either. Revolv costs $99 per year, while Instal charges varying fees plus interest.

But what’s the value of a better credit score? Remember, good credit can help you take out a loan, get a credit card, and even secure housing. So, with all that on the line, Revolv and Instal are worth it for lots of people.

Now, what about CS Max, Credit Strong’s most expensive product? Let’s be real – it’s not for everyone. Credit Strong itself admits as much.

But what if you’ve got plenty of cash, and you’re willing to use it to improve your credit? What if credit’s a problem, but capital isn’t? Maybe you’re trying to start a business or get a hefty personal loan, and you know you need a major credit rehab in order to make it happen.

In that case, Credit Strong’s CS Max is the hard-hitting product you need.

Commonly Asked Questions About Credit Strong

What are Alternatives to Credit Strong?

Here are some apps and services like Credit Strong that can help you build credit:

- StellarFi (read this full StellarFi review)

- Dovly (read this full Dovly review)

- Cheese (read this full Cheese Credit Builder review)

- Kikoff (read this full Kikoff review)

- Chime (read this Chime review)

- Cleo (read this Cleo Credit Builder Card review)

- Nevly Money (read this Nevly Money review)

For more ways to fix your credit, check out our comparison of Credit Saint vs Lexington Law, or see if working with the best tradeline companies could be the right credit repair solution for you.

Meanwhile, learn how to budget for non recurring expenses so you can be prepared for unexpected costs going forward.

And to learn which budgeting app could best help you manage your finances and boost your savings, check out these comparisons of Rocket Money vs the competition:

Then use a net worth tracker to see how your new financial strategies are paying off.

Is Credit Strong a Scam?

Credit Strong is a division of Austin Capital Bank, and it definitely isn’t a scam. All of its products are explained clearly on its website, so there shouldn’t be any nasty surprises. Just know ahead of time that the goal should be to build credit, not borrow money.

What is The Catch With Credit Strong?

The only catch with Credit Strong is that the credit builder loan isn’t actually a way to borrow money. The idea is to pay back the loan before you actually get the funds. That’s what makes it a low-risk way to build credit!

Does CreditStrong Actually Work?

Some users report that Credit Strong has helped them improve their credit scores. For example, one reviewer on Trustpilot said their score had increased by 100 points since signing up. And it makes sense since the products help you report on-time payments to the three major credit bureaus.

Is CreditStrong Legal?

Credit Strong is 100% legal. In fact, it’s a division of a reputable bank called Austin Capital Bank, which is a member of the FDIC. This isn’t some sketchy organization operating in the shadows!

Do You Get Your Money Back With CreditStrong?

There are two ways to get your money back with a credit builder loan from Credit Strong:

- Pay off the entire loan

- Cancel the service

In either case, Credit Strong promises to return your money minus the non-refundable administration fee and the interest on the loan.

Is CreditStrong The Same as Self?

Credit Strong and Self are similar services, both using credit builder loans to help boost your credit score. That said, they offer slightly different plans and products. For example, Credit Strong offers a revolving line of credit, while Self offers a secured credit card.

See how much you could save by learning how to cancel all subscriptions on your debit card or credit card.

Does Credit Strong Give You Money?

Credit Strong doesn’t “give you money” in the way that a typical loan does. Instead, you make payments upfront and then get most of the money back as savings. This is called a credit builder loan, and it’s designed to increase your credit score, not give you access to funds.