Affirm Reviews – Pros and Cons in 2025

By Maddy Scheckel

By Maddy Scheckel We’ve all been there.

That sinking feeling when your dying laptop crashes again, and you can’t afford a new one.

You finally paid off your credit card balance only to build it back up again.

Considering the average annual credit card fee is roughly $94 per card, here’s how you can avoid plastic and discover a cheaper way to pay.

Affirm is a buy-now-pay-later (BNPL) service that offers little to no interest loans without fees. This means a brand-new laptop could be yours in only four payments.

I’ve taken the time to research the app and scour through the online Affirm reviews. So, keep reading to find out how Affirm can work for you.

What Is Affirm?

Affirm is an installment loan app with interest rates as low as 0%, so you can buy something now and pay later (BNPL) without a credit card.

It has partnerships with big names like Amazon, Peloton, and Walmart and is available at over 235,000 stores, both online and in-person. Plus, Affirm now has a Google Chrome browser extension, so you can use the BNPL option wherever you shop online.

Affirm’s maximum purchase amount is $17,500, and they offer two pay structures:

- Pay-in-four plan (Split Pay)

- Monthly pay plan

Source: Affirm

No hidden extras – with both payment options, you’ll know precisely how much you need to pay for each installment before you make a purchase. Affirm doesn’t charge late fees, but be mindful that late payments may negatively impact your credit score.

Simple interest (no deferred interest) – your payment schedule is the same throughout your payback period. The interest rate depends on the retailer and can range from 0% up to 30%. Some brand names that charge no interest include Figs, Room & Board, and Casper.

Even More Options – Affirm is best known for its BNPL plans, but that’s not all they offer. They have a single-use virtual card option you can use to pay for purchases at stores not listed on their website. And for loyal Affirm users, they now offer a Debit+ card that links straight to your bank account.

How To Use Affirm

A quick and easy way to access Affirm is through online shopping. Many retailers have the app integrated into their checkout process, so you can opt-in to an Affirm payment plan directly on the retailer’s website.

You can also open an account with Affirm through their app. There, you’ll get prequalified and be given a maximum spending limit (up to $17,500).

But remember that despite your spending limit, Affirm requires pre-approval for every purchase you make. This goes for either of the payment options you choose. Not to worry, though; approvals usually only take a few minutes.

Source: Affirm

Affirm Option 1: Split Pay

If you use Split Pay, Affirm will divide your purchase amount into four even payments without interest.

Say you buy a Chromebook for $800. You’ll pay $200 at the checkout, and then Affirm will charge your debit card, checking account, or credit card (whichever you used to buy the device) $200 every two weeks until you’ve paid the full $800 off after six weeks.

Affirm Option 2: Monthly Pay Plan

If you’re worried you can’t meet the Pay-In-Four plan payments, you can opt for the Monthly Pay plan and spread out your payments over a more extended period, from 3 to 60 months.

This option may seem cheaper, but these plans typically charge higher interest, up to 30% APR, depending on the merchant. So you’ll end up paying more, but it will be spread over a longer period.

Note: You may have to make an initial payment at checkout if you don’t qualify for a loan to cover the entire purchase amount.

Is Affirm Legit?

Yes, Affirm is a reputable provider of BNPL loans. Loans provided by Affirm Loan Services, LLC, are made under state law. Also, other lending partners may supply loans through Affirm as it is a publicly-traded company (on NASDAQ as AFRM) with a market cap of $4.93 Billion as of November 2022.

Affirm also works with a broad network of retailers, including Target, Nordstrom, and Walmart, and brand names, such as Williams Sonoma and American Airlines.

Is Affirm Safe?

Affirm is a safe way to borrow money and keep control over your debt. Unlike credit cards, Affirm doesn’t supply you with a revolving line of credit. Instead, it checks if you qualify for its payment options each time you want to buy.

And unlike credit cards with variable APR rates, their payment options are transparent. This way, you will always know how high your payments will be before you buy.

Also, unlike some BNPL providers, Affirm doesn’t charge any fees (late, penalty, or annual). But late payments can affect your credit score and chances of getting future loans.

If you need help fixing your credit, check out our comparison of Credit Saint vs Lexington Law, or see if working with the best tradeline companies could be the right credit repair solution for you.

And if you want to make payments on your purchases without impacting your credit score, check out these no credit check shopping sites.

Meanwhile, learn how to budget for non recurring expenses so you can be prepared for unexpected costs going forward.

If you get paid twice a month and are struggling to account for that in your budget planning, learn how to budget biweekly paycheck. And if you need to ramp up your savings fast, learn how to save $3000 in 3 months.

As with any loan, think before you click. Read below for some do’s and don’ts to keep in mind. And always read the fine print.

Do’s:

- Use only if you need to buy an expensive item, like a MacBook for college. Those sweet Air Jordans? Save up and pay cash.

- Say yes to Affirm when you can’t get a credit card or haven’t built up a solid credit history. Good to know: Unlike most personal loans, Affirm only does a soft credit pull to check your credit score.

- Take the zero-interest option; it’s the best value for money, provided you can make payments.

- Affirm is for you if you want to control how much you pay in installments.

- Go for it if you like to pay loans off early; Affirm doesn’t charge a prepayment penalty.

Don’ts:

- Are you an impulsive buyer? Pay cash for things you don’t need, and don’t buy things you want immediately. Avoid all BNPL services.

- Stay clear if you need flexibility in payment options down the line. Affirm won’t let you reschedule or pause a payment.

- Affirm is not a good option if you struggle with credit card debts. Pay these off first.

- Use Affirm to build credit. This company only sometimes reports payment history to Experian for loans, but this isn’t guaranteed. Rather, if you need to build credit, consider taking out a personal loan instead.

Affirm Reviews

As with any money lender, it’s always a good idea to check what other customers say before taking the plunge. I’ve gathered reviews from several sites. Here are the ones I found to be most helpful:

Positive Affirm Reviews

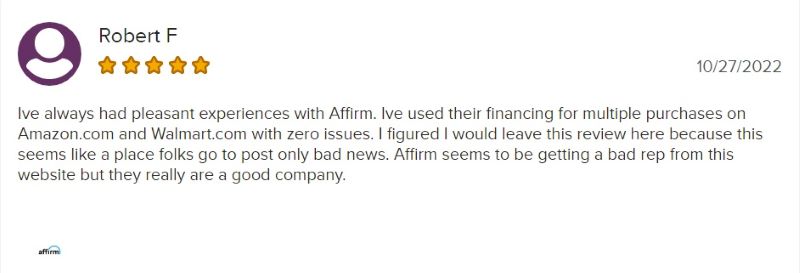

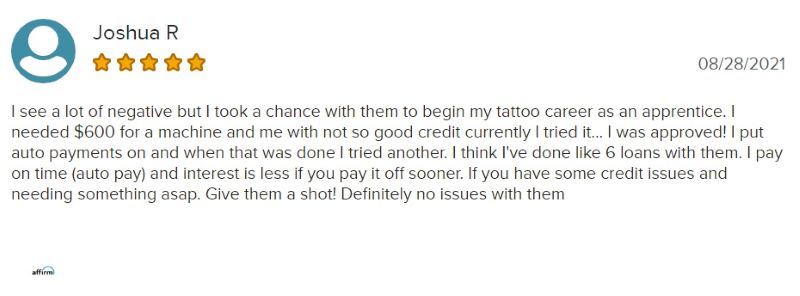

Here’s what two Affirm users posted on the International Association of Better Business Bureaus review website:

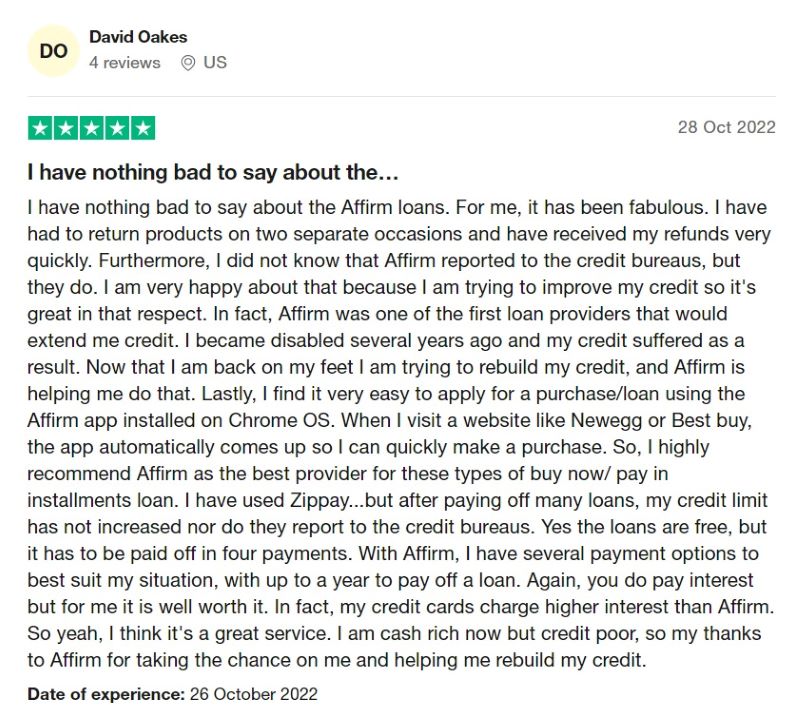

Check out what another user had to say on Trustpilot’s review website:

Negative Affirm Reviews

Here’s what an Affirm user posted on the International Association of Better Business Bureaus review website:

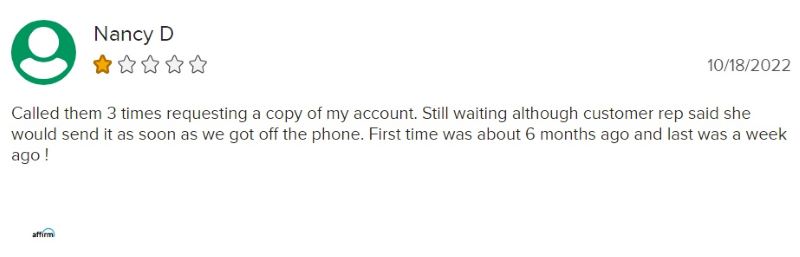

Check out what another user had to say on Trustpilot’s review website:

Commonly Asked Questions About Affirm

Affirm Vs. Afterpay

While both companies provide buy-now, pay-later (BNPL) loans, Affirm is usually a better fit for most people because:

- Affirm offers multiple payment options.

- It doesn’t charge late fees (Afterpay’s late fees can be up to 25% of the purchase price).

- Affirm can help build credit when you pay on time.

Is Affirm Com Trustworthy?

Yes, it’s a legit company offering buy-now, pay-later (BNPL) loans for amounts up to $17,500. So far, it has 12.7 million customers, with 10.5 million total transactions to date.

Can Affirm Hurt Your Credit Score?

It depends. Affirm doesn’t report loans with only a 0% APR and four biweekly payments. Affirm only reports the loan history of their other loans to Experian, and late payments may affect your credit score.

To learn which budgeting app could best help you manage your finances and boost your savings, check out these comparisons of Rocket Money vs the competition:

Then use a net worth tracker to see how your new financial strategies are paying off.

If you’re looking for a low-tech, hands-on budgeting method, learn about cash envelope categories. And if you need to boost your savings fast, the 60/30/10 rule budget can help.

How Does Affirm Work?

Affirm is a loan financing company providing BNPL loans. Here’s how it works:

- Open an account through the app.

- Receive prequalification & a spending limit of up to $17,500.

Or

- Pick Affirm as a payment option when shopping online.

- Apply for a one-time virtual card to shop in regular stores.

What Are The Cons Of Affirm?

Here are a few common cons of using Affirm:

- Some monthly plans charge 30% APR.

- Customer service can be unreliable.

- Prequalification doesn’t mean approval for every transaction.

- Have any late payments? It may be hard to get another loan.

- Affirm may require a down payment.

Is Affirm Like A Credit Card?

No, Affirm is not a credit card. Here are three key differences. Unlike credit cards, Affirm doesn’t:

- Provide a revolving line of credit.

- Charge interest on top of interest.

- Include a penalty fee on its 0% APR promotions.

Does Affirm Affect Credit?

Sometimes. Affirm does not report all loans to Experian, but it does some. In that case, you build your credit each time you pay on time. But paying late may lower your credit score. Also, every Affirm loan you take out shows up as a separate loan.

Is Using Affirm A Good Idea?

It can be if you’re looking for quick and easy financing for an essential item with no hidden fees or extras. With Affirm, you know your actual payments, and you can even make early payments without a penalty. But it’s not entirely risk-free. Avoid it if you’re an impulsive buyer.

What Credit Score Do You Need For Affirm?

According to Affirm, you’re more likely to be approved if your credit is 640 or higher. But if your credit score is lower and you want to improve it, a personal loan for bad credit might be a better option.

What are Affirm Alternatives?

- Sezzle (read full Sezzle review here)

- Perpay (read this full PerPay review to learn more)

- Afterpay (read these Afterpay reviews to learn more)

- Zilch (read this full Zilch review to learn more)

- Nelo (read this Nelo review to learn more)

- Klarna (read these Klarna reviews to learn more)

- Zip (read these Zip reviews)

- PayPal Pay in 4 (read these PayPal Pay in 4 reviews to learn more)

- Splitit (read this Splitit review to learn more)

- Apple Pay Later (read this Apple Pay Later review to learn more)

- Sunbit (read this Sunbit review to learn more)