Hometap: A New Way To Access Your Home Equity

- Investment Amount: Up to 25% of a property’s value or a maximum of $600k

- Eligible Properties: Single-family homes or condos

- Term Length: 10 Years

- How To Settle: Sell the property, buy out Hometap’s original investment, or take out a home equity (or other) loan

- Applicant Requirements: A minimum FICO score of 500 and a minimum of 25% equity in a property

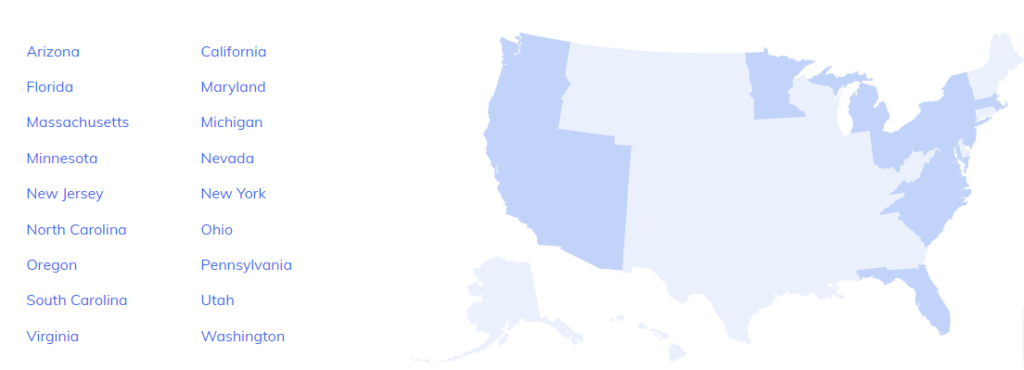

- State Availability: AZ, CA, FL, MD, MA, MI, MN, NV, NJ, NY, NC, OH, OR, PA, SC, UT, VA and WA

As a homeowner, every monthly mortgage payment you make helps you build the equity you hold in your home. And with the record-high rise in property values over the last two years, many homeowners may now find that their house is their most valuable asset. So what’s the best way to tap into it for cash?

You probably already know about a home equity loan and home equity line of credit, both of which require you to take on more debt and make ongoing monthly payments to pay it back. But what if there was a way to access the equity in your home without having to do that? This is exactly what Hometap offers.

What Is Hometap And How Does It Work?

Founded in 2017 by Jeffrey Glass, Max Campion, Charlie Vrettos and Andrew Vassallo, Hometap was created to provide homeowners with an easier way to access the wealth they hold in their homes.

Instead of choosing between a second mortgage or a complex revolving line of credit, Hometap offers what’s called a home equity sharing agreement, also known as home equity investments. Hometap will invest in your home, offering you a lump sum of cash today in exchange for a share in your home’s future value. Your house is 100% still yours, to live in and make memories, to redesign and remodel. However, investment agreements are tied to 10-year terms, by the end of which a homeowner must settle.

There are three ways to do this:

- Sell your home and give Hometap its share of the profits

- Buy out Hometap’s investment with your own money

- Take out a home equity (or other) loan to pay back the investment

Can Anyone Apply For A Hometap Investment?

Hometap offers investments amounting to 25% of a property’s value or a maximum of $600,000. To apply, you need to have a minimum FICO score of 500 — though a score of over 600 is ideal – and have at least 25% equity in your property.

Hometap only invests in properties that are single-family homes or condos and they must be located in one of the following states:

The Application Process

If you’re curious about a Hometap home equity investment, you can get a quote in less than two minutes on Hometap’s website.

- If you want to move forward, create an account and complete an investment inquiry.

- If you qualify, a Hometap investment manager will send you an estimate and schedule a time for a call to go over numbers and answer any questions you may have about the application process.

- Apply. The entire application takes about 20 minutes to complete — additional documents will be needed to complete the application, so have them ready in advance.

- Next comes the home appraisal. Hometap will schedule a time with you to have a third-party appraiser evaluate your property.

- After the appraisal, the investment details will be finalized, and the agreement will be sent to you for signing.

- Once signed, funds are typically sent within a few days.

Overall, the whole process can take a couple of weeks.

The Pros And Cons Of A Hometap Home Equity Investment

Pros

- A home equity agreement is not a form of debt. You won’t owe any interest on the money you receive, and you don’t have to pay it back.

- Once a Hometap agreement is signed, you’ll receive the funding typically within 4 to 7 days. Once you get the cash, it’s yours to do whatever you want with it.

- You don’t need to have perfect credit to apply. Hometap works with people in different credit brackets, from poor to great.

- You have various options for settling an agreement – sell your home or buy out Hometap with your own money or via a loan.

- For the most part, there are no income requirements as long as you have enough equity in your home and meet credit requirements.

Cons

- A home equity agreement could cost you more than a loan would if your property were to appreciate by a significant amount. Hometap’s profit share or the cost to buy them out could be very high.

- There is a 3% service fee, which is deducted directly from the investment amount. And Hometap notes that other out-of-pocket costs accrued from things like the appraisal, escrow, attorney or notary fees, document recording and more.

- If at the end of the 10-year term you wanted to keep your house and are unable to find another way to pay Hometap its share in full, you may be forced to sell your home. If you are unable to pay Hometap at all, you risk losing your home altogether.

Is Hometap The Right Choice For You?

If you’re trying to avoid monthly payments that can inconvenience you and disrupt your day-to-day finances, Hometap is a great option.

New homeowners should wait a couple of years before considering a home equity investment because you may not have enough equity in your house to qualify for one – you need to have 25% equity for Hometap.

Any homeowners who bought their house with the intention of making it their “forever home” may want to consider another option. After all, you will have to pay Hometap back by the end of your 10-year term. And if you cannot come up with the cash Hometap is owed on your own or by other means, you may be forced to sell your house. However, if the property is a starter home, then Hometap and other companies like it may very well be the best option for accessing the equity you have in it.

Whatever method you choose for accessing your home equity, consider your financial situation carefully, and bear in mind things can change in the future.