Hometap Vs Unison Vs Unlock: What Is The Best Way To Tap Home Equity in 2024?

By John Boitnott

By John Boitnott You’ve been making your mortgage payments for several years, and you’re at a point where you can harness the equity in your home to increase your purchasing power.

But maybe the thought of going into even more debt doesn’t exactly light you up with excitement.

American homeowners currently hold over $30 billion in equity, but what options are available when those homeowers need cash? There are more than you might think, and one you may not be familiar with is a home equity agreement.

This alternative for tapping your home’s equity is gaining popularity with homeowners who either don’t meet the qualifications of a traditional home equity loan or don’t want to take on any additional debt.

Let’s look at Hometap vs Unison vs Unlock and see the kinds of homeowners who can benefit from these home equity agreement providers. Maybe you’ll want to jump on the deal and get started with one of them today.

Hometap Vs. Unison Vs. Unlock

| Company | Hometap | Unison | Unlock |

| Equity amount available | Up to $600,000 or 25% of your home’s value | Up to $500,000 or 17.5% maximum investment range | Up to $500,000 |

| Fees | 4.5% of the investment amount plus appraisal, title, and government recording fees. | 3.9% of the investment amount plus appraisal fees and settlement costs (title, taxes, recording fees) | 3.9% of the investment amount plus appraisal and inspection fees |

| Term | 10-year term | Flexible 30-year term | 10-year term |

| Max loan-to-value ratio (LTV) | $15,000-$600,000 LTV maximum of 75% | $30,000-$500,000 LTV maximum of 70% | $30,000-$500,000 LTV maximum of 70% |

| Minimum credit score needed to apply | 550 | 620 | 500 |

| States available in | Arizona California Florida Michigan Minnesota Nevada New York New Jersey North Carolina Ohio Oregon Pennsylvania South Carolina Utah Virginia Washington D.C. | Arizona California Colorado Delaware Florida Illinois Indiana Kansas Kentucky Massachusetts Michigan Minnesota Missouri Nebraska Nevada New Jersey New Mexico New York North Carolina Tennessee Utah Virginia Washington D.C. Wisconsin | Arizona California Colorado Florida Michigan New Jersey North Carolina Oregon Pennsylvania South Carolina Tennessee Utah Virginia Washington |

| Other qualifications | – 25% equity in home – Own a single family home or Condo/apartment, Multi-family home (1-4 units), Manufacctured home – Investment is up to 25% or less of total home value | – Owner occupied primary residence with built up equity – Single-family homes, townhouses and condos – Plan to stay in your home for a recommended 5 years – Investment in a second home/vacation home is possible | – 20% equity in the home – Single family homes or rental properties (with rent verification) are eligible |

Hometap At A Glance

|

Fees |

3% of the Investment amount, plus appraisal, title, and government recording fees. |

| Qualifications | Single family, Condo/apartment, Multi-family home (1-4 units), Manufactured home; 25% equity in the home; investment amount is 30% or less of total home value. |

| Minimum Payment Amount | No monthly payments |

| Available Equity Amounts | 5% to 15% range |

| Credit Score Requirements | 620 or higher (can apply with a score as low as 500) |

| Hometap operates in 16 states |

|

| Length of Loan Terms | 10-year term |

| Max loan-to-value ratio (LTV) | $15,000-$600,000

LTV maximum of 75% |

Unlock At A Glance

|

Fees |

3% of the investment amount plus appraisal and inspection fees |

| Qualifications | Homeowners need to have minimum equity of 20% of the home’s value.

Single family homes or rental properties (with rent verification) are eligible. |

| Minimum Payment Amount | No monthly payments |

| Available Equity Amounts | 1% to 43.5% |

| Credit Score Requirements | 500 or higher |

| States Where Service Is Available |

|

| Length of Loan Terms | 10-year term |

| Max loan-to-value ratio (LTV) | $30,000-$500,000 |

Unison At A Glance

|

Fees |

3.9% of the investment amount plus appraisal fees and settlement costs (title, taxes, recording fees) |

| Qualifications | House must be an owner-occupied, primary residence. Can include single-family homes, townhouses, and condos. In some cases, investment in second homes/vacation homes is possible. |

| Minimum Payment Amount | No monthly payments |

| Available Equity Amounts | 17.5% maximum investment range |

| Credit Score Requirements | 680 or higher |

| States Where Service Is Available |

|

| Length of Loan Terms | Flexible 30-year term |

| Max loan-to-value ratio (LTV) | $30,000-$500,000

LTV maximum of 70% |

What Are Alternative Ways To Get Equity Out Of Your Home?

There are several different ways homeowners can harness the purchasing power of the equity in their homes. And each has its benefits and drawbacks.

You may have parents or grandparents who used a reverse mortgage to get the extra cash they needed for home renovations, vacation money, or paying off debt.

Reverse mortgages are typically settled when the mortgage holder passes away and the house is sold. The balance was then paid and the remainder of the home’s proceeds from the sale went to the estate’s beneficiaries.

The loan balance on the reverse mortgage may have grown over time, but the home also appreciated in value. This helped offset the balance owed. It benefitted the homeowner while alive, and the beneficiaries when the property was sold.

One drawback of a reverse mortgage is that if you’re not at least 62, you don’t qualify for one. If you need money now, you need to look elsewhere.

Refinancing is an option and one that made sense when interest rates were so low they were near zero in some cases. But interest rates are starting to climb, and are showing an upward trend for the foreseeable future.

There’s also the HELOC (Home Equity Line Of Credit) option. This is effectively a second mortgage and amounts to additional debt that many people want to avoid.

Home equity agreements are an option for people who either can’t qualify for a standard home equity loan or who want to tap into their real estate equity without adding to their debt. The popularity of these is evident by the number of companies offering this product. Let’s take a look at three companies offering this creative way to get cash out of your home’s equity.

What Is Hometap? How Does Hometap Work?

Hometap offers homeowners a way to tap the equity in their homes (hence the name) for cash. The homeowner begins the process by filling out a Hometap investment inquiry on their website.

If Hometap determines that the home is investable, an investment manager will send the homeowner an estimate of the terms and set up a call to discuss the specifics of the application process and potential agreement.

Then a physical appraisal of the property will be done to determine the home’s current fair market value. Once the appraisal and application process is completed and approved, the signing of the agreement and funds transfer can occur.

Like Unison, the term of the equity agreement lasts 10 years, and the homeowner has the option to buy out the agreement before the term is up.

One of the things that differentiate Hometap from other equity sharing agreement companies is that they offer their services to homeowners with lower credit scores. If a homeowner has a credit score as low as 550 (considered “subprime” by most mortgage companies), they can apply for an equity sharing agreement through Hometap. However, Hometap recommends a credit score above 600.

Hometap also offers renovation adjustments to a home’s value if the renovation costs $25,000 or more.

Here’s a short video breaking down how it works:

Is Hometap Legit?

Hometap operates in 16 states. They have received overwhelmingly positive reviews. It has an A+ rating from the Better Business Bureau, a rating of 4.9 on Trustpilot (based on 3,332 reviews), and has been accredited since 2019.

What Is Unlock? How Does Unlock Work?

Unlock, much like Unison and Hometap, pays a homeowner cash in exchange for a share in the proceeds when the home is sold. As it is not a loan, there are no monthly payments. When the home is sold, the agreement is settled. The homeowner pays back the original investment amount, and Unlock shares in any increased value, or shares the loss if the home’s value declines.

Like Hometap, Unlock offers homeowners with low credit scores the opportunity to apply for an equity sharing agreement. Unlock’s minimum FICO score is 500, and a score this low may require verification of income.

Unlock uses independent appraisers to determine a home’s fair market value. Unlock also uses home inspectors where applicable to determine the condition of a home.

Homeowners can apply online. Unlock requires that you upload documentation such as insurance declarations, mortgage statements, and various forms of identification. Once the application is completed, an appraisal is scheduled if the property is investable. Signing and fund transfer takes place shortly after.

Unlock offers the homeowner to chance to buy out the agreement either completely or partially. An appraisal is done at the time of the buyout to determine the home’s market value at that time.

This short video from Unlock could help you decide whether unlocking your home’s equity with Unlock could be the right move for you right now:

Need cash now but struggling with your low credit score? Unlock can help.

Is Unlock Legit?

Unlock is a legitimate equity-sharing company. Unlock operates in 14 states, the fewest of the three companies reviewed here. Unlock has been reviewed positively by customers. It has an A- rating on the BBB and has been accredited since 2021.

What Is Unison Home Equity? How Does Unison Work?

Unison provides homeowners an alternative by converting part of their existing home equity to cash without making monthly payments. Unison provides the homeowner with a cash payment in exchange for a percentage share in your home’s future value.

What this means for the homeowner is If the house goes up in value, Unison shares in the gain as a co-owner of the home. If the home goes down in value, Unison also shares in the loss. Unison determines the home’s fair market value by getting an independent appraisal.

The homeowner settles the investment with Unison when the home is sold. The homeowner pays Unison the amount of the original home equity investment, plus or minus the previously agreed-upon share of your home’s change in value. That’s where the company potentially makes its money in the process.

Unison also offers the homeowner the option of buying out their share after a restriction period but before the 10-year agreement term is finished. If the homeowner exercises that option, an appraisal will be done to determine the home’s current fair market value. In a buyout, Unison does not share in losses if the value goes down.

Here’s a video breaking down how Unison works:

Is Unison Legit?

Unison is a legitimate way to get money out of the equity in your home. Unison operates in 30 states, which is the most of the three companies reviewed here. It has an A+ rating from the Better Business Bureau as of the date of writing and has been accredited with the site since 2013.

Real Reviews From Real Users For Unison, Hometap, and Unlock

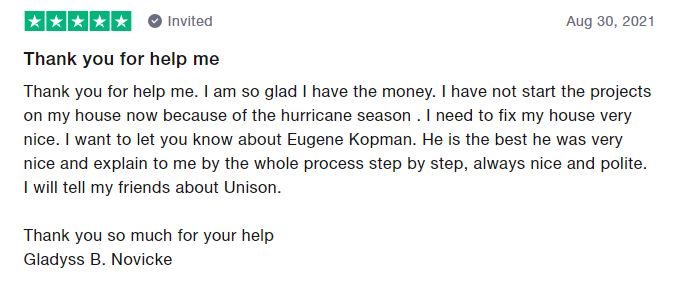

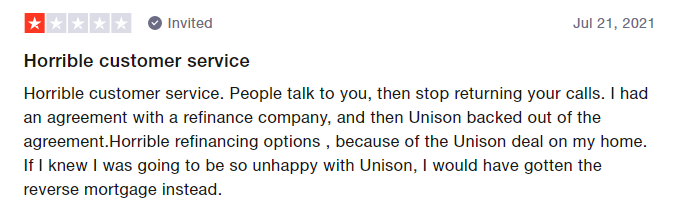

Unison Reviews

Unison has a total of 46 reviews on TrustPilot. 70 percent of these reviews are rated as 5 stars or excellent. Excellent reviews focus on the ease of Unison’s application process and the friendliness of the representatives, often mentioning them by name.

Negative reviews mention the lack of customer service after the agreement is signed and difficulties with refinancing.

Hometap Reviews

Hometap has 924 reviews on TrustPilot. 91 percent of those are rated as 5 stars or excellent. Excellent reviews mention the strong service when applying for an agreement, often mentioning reps by name.

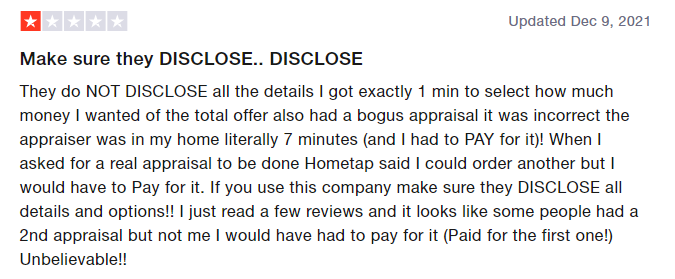

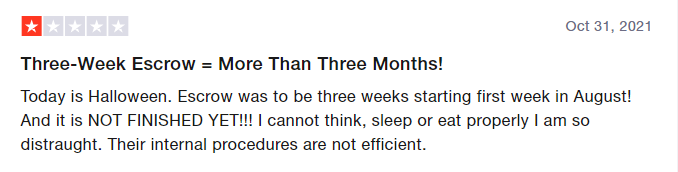

Negative reviews mention late disclosure of information, dissatisfaction with appraisal values, and delays in escrow.

Unlock Reviews

Unlock has 95 reviews on TrustPilot. 82 % of those reviews are rated as 5 stars or excellent. Like Hometap and Unison, positive reviews mention the ease of the application process and, again, mention customer service people by name.

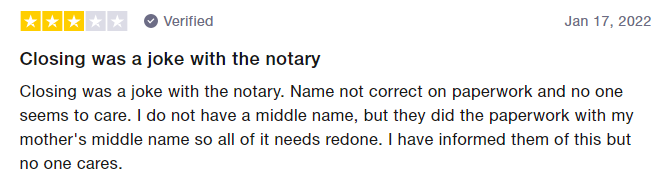

Negative reviews seem to express dissatisfaction with third parties involved in closing.

Important Differences Between Hometap, Unison And Unlock

While Unison, Hometap, and Unlock have similar business models, application processes, and procedures, there are some important differences between them.

Unison targets homeowners with higher credit scores while Hometap and Unlock offer those with lower credit scores the opportunity to apply. While there are no monthly payments involved with an equity sharing agreement, the homeowner is still responsible for making payments on both the mortgage and insurance policy. So the ability to pay is an indirect but important consideration.

Also, Unison is the most widely available as it operates in 30 states. Hometap operates in 16 states and Unlock operates in 14.

Hometap vs Unlock

Hometap and Unlock both allow you to tap into your home’s equity even if you have a lower credit score (minimum of 500), and both offer a 10-year term.

As mentioned, Hometap operates in 16 states while Unlock operates in 14. Let’s explore the differences between these two further so you can decide between them if both are available in your state.

One of the biggest differences is in the fees you’ll pay. Unlock charges 3.9% of the investment amount plus third-party fees vs. the 3.5% plus third-party fees charged by Hometap.

But while Hometap wins in the fees category, Unlock comes out ahead in the amount of equity you need. Hometap requires 25% while you only need 20% to qualify with Unlock.

What These Home Equity Loan Companies Excel At

All three companies excel at making their application process efficient and communicating with the customer throughout that process. Each company and its individual representatives are praised in customer reviews.

Hometap Pros And Cons

- Available to those with lower credit scores

- 10 year term with option to buy out early

- Maximum loan value of $600,000

- Only available in 15 states

Unlock Pros And Cons

- Available to those with lower credit scores

- 10 year term with option to buy out early.

- Offers partial buyouts

- Rental properties are eligible with rent verification

- Only available in 15 states

Unison Pros And Cons

- Operates in 30 states

- Terms can go up to 30 years

- Option to buy out early

- Not available to those with lower credit scores.

Bottom Line: Which Home Equity Option Is Best For You?

Factors to consider when selecting which company to work with include credit score, loan term, and location. Unison operates in most states, but requires the highest credit score. Hometap and Unlock operate in fewer states but offer agreements to those with lower credit scores.

Hometap and Unlock’s agreement terms are fixed at 10 years, but Unison offers terms up to 30 years.

FAQs

What does Hometap cost?

Hometap’s agreement is settled when the homeowner pays back Hometap’s initial investment, plus a share of the increase in the home’s value once sold. If the home decreases in value, Hometap shares the loss.

Closing costs involve a 3.5% fee plus any third-party costs (appraisal, title, recording fees, etc.)

Where is Hometap available?

Hometap is available in 16 states:

- Arizona

- California

- Florida

- Maryland

- Massachusetts

- Michigan

- Minnesota

- New Jersey

- New York

- North Carolina

- Ohio

- Oregon

- Pennsylvania

- Virginia

- Washington

Is Unlock a reverse mortgage?

Unlock is not a reverse mortgage. The minimum age for a reverse mortgage is 62. Unlock offers equity sharing agreements to homeowners of all ages.

What is the catch with Unison?

Unison is not available to homeowners with a credit score of less than 680.

So what do you think? Get started with one of these companies to hack your home equity. Start today with Hometap, Unison, or Unlock.