Fundrise vs Groundfloor [2025] Groundfloor vs Fundrise

By Maddy Scheckel

By Maddy Scheckel What’s the best way to invest your money? According to a recent poll, 34% of Americans say the answer is real estate.

You might be thinking, “But buying a property is super expensive!”

True, but you can still get involved in real estate. The key is to use investment platforms like Fundrise and Groundfloor.

Below, I’ll walk you through a detailed Fundrise vs Groundfloor comparison. Both companies offer accessible real estate investments, but there are some major differences.

Fundrise vs Groundfloor Overview

Fundrise and Groundfloor are investment platforms that let you pool your money with other people so you can invest in real estate.

Both platforms prioritize accessibility. You can use them even if you’re not an “accredited” investor, and the minimum investments are small – $10 with Fundrise and $100 with Groundfloor.

But that doesn’t mean the platforms are the same. Each one has its own business model. Fundrise lets you buy into a portfolio with actual real estate properties, while Groundfloor lets you fund loans that other people use to invest in real estate.

If you want to start investing but need to learn more about the basics, check out our guide to investing for beginners.

What is Fundrise and How Does Fundrise Work?

Fundrise is an investment platform that lets you buy into a massive real estate portfolio.

You don’t need to be an accredited investor to open a Fundrise account, and the minimum investment is just $10.

Real estate investing is Fundrise’s main interest, and it’s super relevant to the Fundrise vs Groundfloor debate – so that’s what I’ll focus on here. But Fundrise also offers investments in private credit and venture capital.

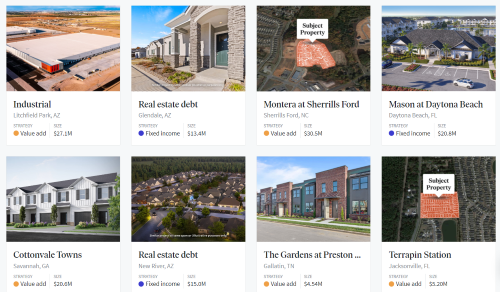

Fundrise buys and manages a bunch of properties – currently 290. As an investor, you buy into the portfolio, which is worth over $7 billion in total.

Source: Fundrise

If the portfolio makes money, you’ll get a share of the returns. And if the portfolio loses money? You guessed it – you’ll face your share of the losses. No one ever said real estate investing was risk-free.

But here’s the good news: Fundrise investors generally make more money than they lose. That’s probably why the platform has attracted more than 2 million users over the years.

Here’s how to get started:

- Create a Fundrise account online. You can choose to open a standard “Individual Brokerage Account” or opt for an Individual Retirement Account (IRA).

- Invest in the real estate trust (or make other investments). This step should be simple and easy thanks to the user-friendly Fundrise mobile app.

- Collect your returns (if your investments earn money). Fundrise will send you your earnings every quarter.

An investment in Fundrise’s real estate portfolio is meant to last 5 years. Getting your money out earlier can be difficult. You might have to pay a penalty (1% of total share value), and you’ll have to wait until the end of the quarter for the money to arrive.

So, remember that Fundrise is an “illiquid” investment. You can’t pull out your funds at a moment’s notice. This is just the way this type of investment works.

And if you prefer to take a more active role in your Fundrise investments, for $10 a month, a Fundrise Pro membership gives you full control of your investment portfolio. You’ll be able to create custom investment plans and invest directly into all available funds on the platform, including limited-access, strategy-specific funds.

Learn more about the platform in this complete Fundrise review.

What is Groundfloor and How Does Groundfloor Work?

Groundfloor is a lending platform that lets regular folks invest in real estate projects with as little as $100.

With Groundfloor, you’re not buying into a property itself. Instead, you’re helping to lend money to someone who’s buying the property. Oftentimes, the borrowers are hoping to “flip” a home – meaning they’ll buy it, fix it up, and then sell it for more than they originally paid.

To understand how Groundfloor works, it might be easiest to imagine the flipper’s perspective.

Let’s say there’s a person out there who wants to buy a property and flip it, but they don’t have enough money to make a purchase. So, they decide to get a loan. Groundfloor acts as a lender, offering this person the money they need. But Groundfloor itself doesn’t cough up the money. That’s where you (the investor) come in!

As an investor, you’ll help fund a Groundfloor loan. So, your money, along with money from other investors, would go to the person who’s trying to flip a property for profit. This person will then have to pay the loan back – with interest, of course. And that interest is where you (the investor) will earn your profit.

Each Groundfloor loan is given a grade from A to G – with A loans being the least risky, and G loans being the riskiest. The G loans, while risky, also have the highest possible rates of return. As with most investing, it’s a matter of balancing risk and reward.

Now you’ve got the general idea. But to really understand the key differences in the Groundfloor vs Fundrise debate, you need to know exactly what Groundfloor’s process looks like from the investor’s end.

So here’s how to invest with Groundfloor:

- Create an account. It’s completely free, and you don’t have to be an accredited investor.

- Add funds to your account. You’ll have to link a bank account digitally.

- Start investing! Again, the minimum investment is just $100.

There are a few different investment options available through Groundfloor:

- Limited Recourse Obligations (LROs) – This is Groundfloor’s flagship product. As an investor, you’ll choose to fund a specific loan (used to buy a specific property).

- Groundfloor Notes – These investments come with the stability of a set repayment date.

- Self-Directed Individual Retirement Accounts (IRAs) – You can use your retirement savings to fund your Groundfloor investments.

- Auto Investments – You can have Groundfloor invest your money for you, which means any income you earn will be truly “passive.”

Groundfloor is a great example of an alternative investment opportunity. And why are alternative investments so appealing? Because they help you diversify your portfolio!

Another alternative investment opportunity you might be interested in is precious metals. Check out our Goldco vs Augusta Precious Metals comparison to learn more.

And if wine and spirits sounds like an intersting alternative investment opportunity, check out our Vint vs Vinovest comparison.

Read this article for more information about alternative investments.

And if you’d like to learn about how AI can help you manage your portfolio, check out our Streetbeat review.

Source: Groundfloor

Fundrise vs Groundfloor Fees

You can’t tackle the Groundfloor vs Fundrise debate without considering fees.

*Spoiler alert: Groundfloor charges investors no fees at all, so they win this segment of the Fundrise vs Groundfloor battle; but does that mean they win overall?

Fundrise Fees

When you invest in real estate with Fundrise, you’ll have to pay two annual fees:

- An annual “advisory fee” of 0.15%

- An annual “management fee” of 0.85%

Add those fees together, and you’re looking at only 1% in total fees per year.

So, imagine investing $1,000 in real estate through Fundrise. You’d have to pay $10 each year in fees.

Is it nothing? No, which is why Groundfloor wins this particular battle in the Fundrise vs Groundfloor debate.

But 1% in annual fees is still a minor expense.

Groundfloor Fees

Ready for the best news you’ll hear all day? Groundfloor doesn’t charge investors any fees! That’s right – none! As in zip, zero, nada!

I know it sounds too good to be true. How does Groundfloor make its money?

Here’s how: By charging borrowers.

Remember, Groundfloor is working with two sets of clients: the people who need loans to buy properties (the borrowers), and the people who fund those loans (the investors, like you). Groundfloor has decided to charge the borrowers a fee of 2.75% – 4.00% while charging investors nothing.

Fundrise vs Groundfloor Returns

Why invest in the first place? To get money, of course! That’s why returns are the most important consideration in the entire Groundfloor vs Fundrise conversation.

Let’s look at how much people tend to make on each platform.

Fundrise Returns

In 2021, Fundrise investors saw an annual return of 22.99%. An amazing return by any standard.

But real estate investments aren’t consistent. Some years are better than others.

Here’s Fundrise average annual returns for the past 5+ years:

- 2024: 5.75%

- 2023: -7.45%

- 2022: 1.50%

- 2021: 22.99%

- 2020: 7.31%

- 2019: 9.16%

So, 2021 was fantastic and 2023 a let down. This is the nature of investing – and of hanging in there.

The good news is that the average annual rate of return over the past 5 years came out to 6.7%. That’s not incredible – but it’s a solid Return on Investment (ROR).

Groundfloor Returns

Groundfloor advertises that its investors earn average annual returns of 10%.

That number is based on the past 8 years of investment performance, and it also considers the projects currently listed on the platform.

But not all investments on Groundfloor will give you 10% returns annually.

When you invest with Groundfloor, you’re funding loans so that you can earn interest. That’s a key difference in the Groundfloor vs Fundrise comparison! So, your earnings are tied to the interest rates for the loans.

The loans on Groundfloor have annual interest rates ranging from 4% to 14%, with the riskier loans generally having higher rates. That means your returns could be significantly higher or lower than 10%, depending on your risk tolerance.

One major perk with Groundfloor is that the returns should be consistent. The borrower will start repaying the loan right away, and you can expect consistent cash flow from your investments within 3 months.

Of course, if the returns were truly guaranteed, everyone would be investing with Groundfloor. When I say there’s “risk” involved, I’m talking about the possibility that the borrower defaults – meaning they can’t repay the loan. If that happens, there’s a chance you could lose your money.

Pros and Cons of Fundrise vs Groundfloor

The Fundrise vs Groundfloor decision isn’t an easy one to make. Both platforms have a lot to love, but they also have some genuine drawbacks.

Pros and Cons of Fundrise

Fundrise Pros

- The minimum investment is just $10. That’s even less than Groundfloor, which has a $100 minimum investment.

- Some years bring incredible returns. In 2021, Fundrise investors earned 22.99%.

- While there are fees, they’re super reasonable. You’ll end up paying just 1% per year in advisory and management fees.

Fundrise Cons

- You’ll lose access to your funds. A real estate investment with Fundrise is “illiquid.” You’re meant to leave the money in place for 5 years – and you could face a penalty if you request an early liquidation.

- There’s a risk of losing money. In 2023, Fundrise investors came out behind by 7.45%.

- You can’t choose to invest in specific real estate projects. With Fundrise, your only option is to invest in a bunch of properties at once.

Pros and Cons of Groundfloor

Groundfloor Pros

- It’s easy to access the platform. You don’t have to be an accredited investor, and the minimum investment is just $100. There are also no fees for investors.

- There are multiple ways to invest. You can pick your own projects to fund or opt for “auto investing” and let Groundfloor choose for you.

- Historical returns are solid. Over the past 8 years, Groundfloor has given investors average annual returns of 10%.

- You can get your money back more quickly than with Fundrise. Most loans have repayment terms of just 6 – 12 months – so as an investor, you’re not making such a long-term commitment.

Groundfloor Cons

- You can lose your money in the case of a default. If the borrower fails to repay their loan, you could end up with nothing.

- Borrowers could be involved in risky real estate projects. Flipping properties is far from a guaranteed money-maker – and when borrowers are engaged in risky activity, the probability of default increases.

- You’re at the mercy of the borrowers. Your investment depends on the success of the real estate project – but you’ll have no say in how things are managed. It’s all in the borrower’s hands.

Fundrise vs Groundfloor Review

One way to understand the Groundfloor vs Fundrise conversation is by seeing what real users have to say.

Luckily, there are plenty of reviews about these platforms on the review site Trustpilot. None of them directly make a Fundrise vs Groundfloor comparison, but you can still learn a lot about what sets the platforms apart.

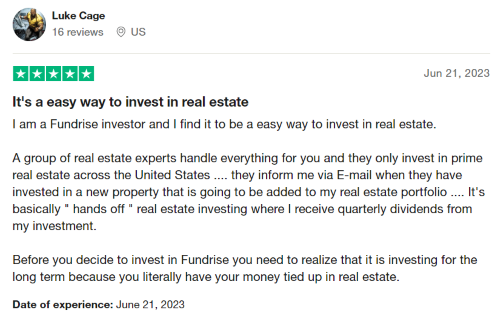

Let’s start with Fundrise. It gets 3.3 stars on Trustpilot.

One user gave Fundrise 5 stars, calling it an “easy way to invest in real estate.” They also offered a useful piece of advice, telling people to accept before investing that Fundrise “is for the long term because you literally have your money tied up in real estate.”

Source: Trustpilot

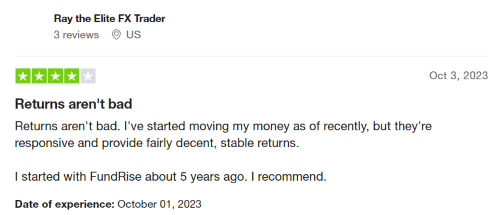

Another user left a 4-star Fundrise review, saying the “returns aren’t bad.”

Source: Trustpilot

But are all Fundrise users happy? Of course not. This is the internet, after all!

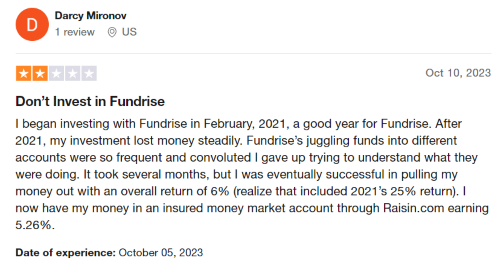

One person left a 2-star review and said, “Don’t invest in Fundrise.” They were annoyed that they only earned a 6% return from their investment.

Source: Trustpilot

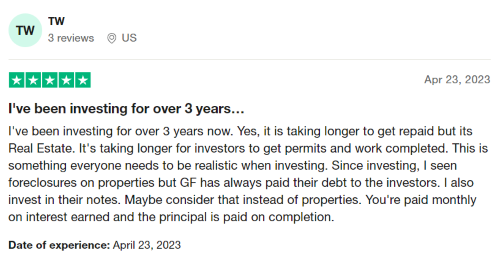

Let’s switch to Groundfloor, which has 4 stars on Trustpilot – meaning it wins this portion of the Fundrise vs Groundfloor debate.

In a 5-star Groundfloor review, someone said they’ve gotten their money back even in the case of foreclosures. That should be super reassuring since foreclosure is a potential risk with Groundfloor’s loan-based business model.

Source: Trustpilot

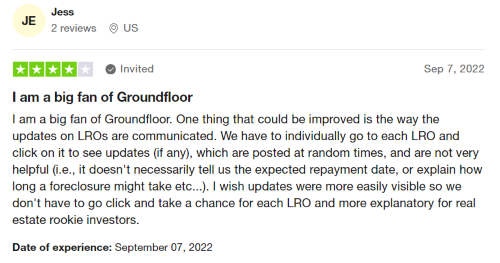

Another user called themselves a “big fan of Groundfloor” in a 4-star review, but mentioned that updates on investments could be more accessible.

Source: Trustpilot

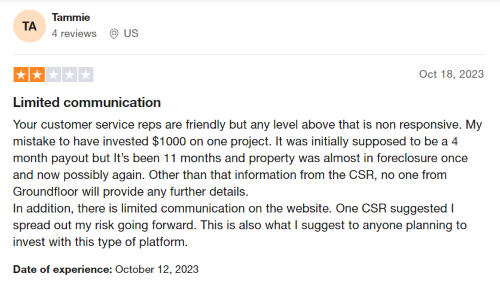

In a 2-star review, a disappointed user complained about the customer service. When an investment underperformed, Groundfloor wasn’t good about providing explanations.

Source: Trustpilot

Fundrise vs Groundfloor Reddit

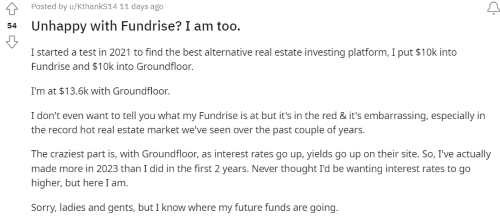

In a recent Reddit post, someone described an experiment they conducted to settle the Fundrise vs Groundfloor debate. They invested $10,000 in each platform. Two years later, their Groundfloor balance had reached $13.6k, while their Fundrise investments had lost money.

The person saw this as a clear sign: In the Groundfloor vs Fundrise boxing match, it was Groundfloor left standing in the ring.

*Note: 2023 was a particularly bad year for Fundrise (investors lost an average of 7.45%), so that most likely had a major impact on this informal experiment.

Source: Reddit

Someone responded by arguing that “3 years is not a good indication of investment performance.” Another person agreed, saying their Fundrise investments had a net annualized return of 15.3%.

Source: Reddit

Another Redditor pointed out that Fundrise and Groundfloor have a “completely different investment profile,” so you have to be careful when comparing the two platforms. This is a useful observation in the Groundfloor vs Fundrise discussion.

Source: Reddit

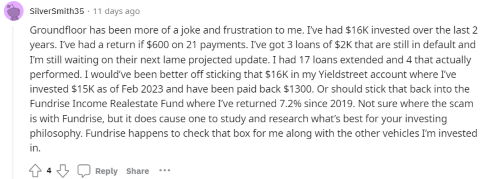

Someone hit back at the original poster by saying they’d had a bad experience with Groundfloor, even calling the platform “a joke and a frustration.”

So yeah – there’s no consensus on Reddit about who wins the Fundrise vs Groundfloor debate!

Source: Reddit

Fundrise vs Groundfloor: Which is Better?

Who wins the Fundrise vs Groundfloor debate?

Drumroll, please.

And the winner is – neither! Because neither platform is obviously better than the other. You just need to decide which is best for you.

Let’s see if you tick these boxes:

- You want to diversify your investment portfolio.

- You’re interested in real estate investing.

- You’re not an accredited investor.

- You don’t have enough money to fund a real estate project of your own.

If that sounds like you, then you’re a perfect candidate for both Fundrise and Groundfloor.

How can you choose between them? Here are two main factors to consider:

- How long do you want the investment to last? Fundrise’s investments involve a 5-year commitment, while a Groundfloor investment could take just 6 months.

- Do you want to own real estate or fund real estate loans? Fundrise’s model lets you buy into a real estate portfolio, while Groundfloor lets you act as a lender.

Now, it’s up to you to weigh your priorities and make an informed decision.

Looking for more investing tips? Check out this article on the best way to invest money.

Don’t Miss This:

Don’t Miss This:

The Hottest Investing Apps Of 2025: Start Building Wealth Today

Commonly Asked Questions About Fundrise vs Groundfloor

What is The Difference Between Fundrise and Groundfloor?

Groundfloor and Fundrise both work in real estate, but they offer different types of investments. With Fundrise, you buy into a portfolio of properties. Groundfloor lets you invest in loans that it offers to outside borrowers investing in real estate.

Can You Really Make Money with Groudnfloor?

You can absolutely make money with Groundfloor. In fact, investors on the platform have earned average annual returns of 10%. Learn more in this complete Groundfloor review.

What is The Downside of Fundrise?

The main downside of Fundrise is that you lose access to your money. Fundrise investments are “illiquid” – meaning you can’t pull out your funds whenever you want. Real estate investments on the platform are meant to last for 5 years.

Fundrise vs Groundfloor vs Concreit?

Fundrise, Groundfloor, and Concreit are all real estate investment platforms, but they have serious differences. With Fundrise, you invest in lots of properties at once, while Concreit lets you pick specific properties. Meanwhile, Groundfloor focuses on funding loans for outside borrowers.